When you buy Bitcoin, sell Ethereum, or earn crypto from staking in Canada, the Canada Revenue Agency (CRA) doesn’t see it as money. It sees it as property. That one shift changes everything when it comes to how much tax you owe-and how badly you can mess up your return.

Over 3.2 million Canadians own cryptocurrency. That’s about 1 in 12 adults. And according to the CRA’s 2025 compliance review, 73% of crypto tax returns had material errors. Most of those mistakes? Wrong cost basis, misclassifying income, or forgetting to report trades on foreign exchanges. This isn’t about being lazy. It’s about confusion. The rules are clear-but they’re not simple.

How the CRA Treats Cryptocurrency

The CRA’s position hasn’t changed since 2013: crypto is not currency. It’s a commodity. That means every time you trade, sell, or spend it, you trigger a taxable event. Buying Bitcoin with CAD? No tax. Holding it? No tax. But swap that Bitcoin for Dogecoin? Taxable. Use it to pay for groceries? Taxable. Even sending crypto to a friend as a gift can be taxable if it’s not truly a personal transfer.

The CRA doesn’t care if you’re a casual investor or a full-time trader. What matters is what you did with the asset. And how you report it.

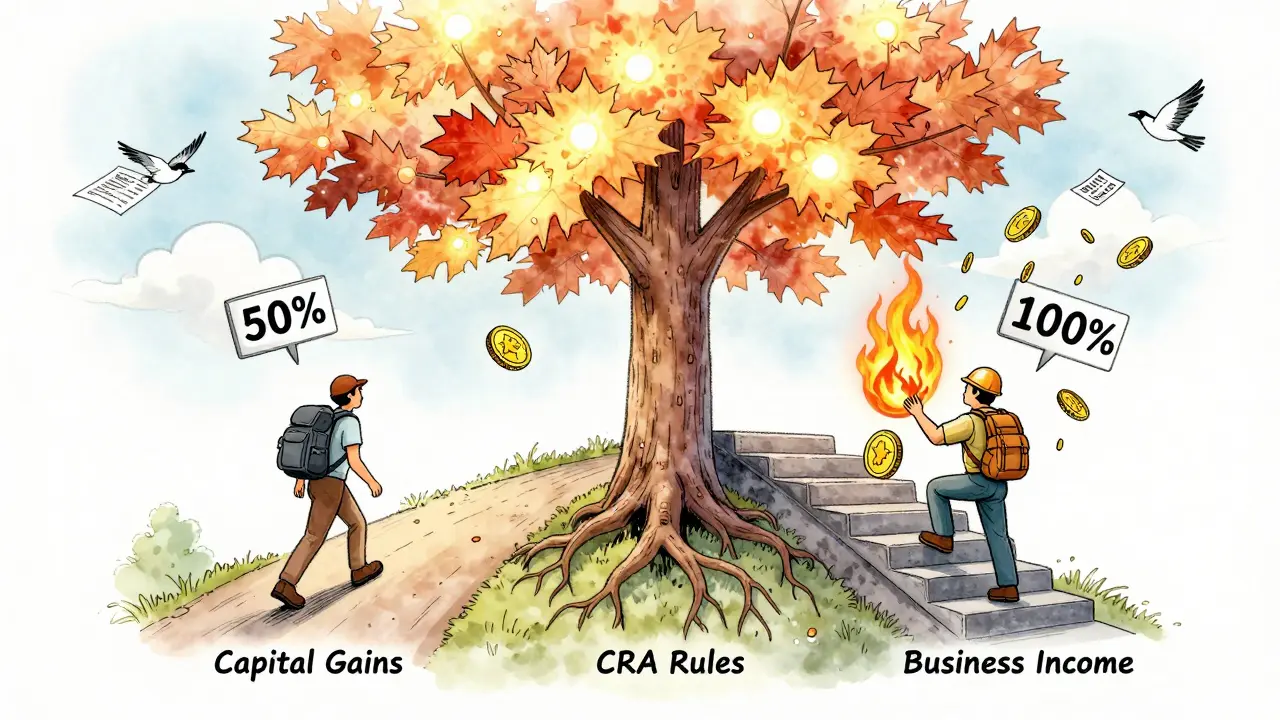

Capital Gains vs. Business Income: The Two Paths

There are two ways crypto income gets taxed in Canada-and the difference could cost you thousands.

Capital gains apply when you dispose of crypto you bought as an investment. That includes selling it for CAD, trading it for another coin, or using it to buy something. Only 50% of the profit is taxable. If you bought $10,000 worth of Ethereum and sold it for $25,000, your gain is $15,000. Only $7,500 counts as income.

Business income kicks in when crypto is part of your regular income stream. This includes mining, staking rewards, airdrops, or being paid in crypto for services. Here, 100% of the value at the time you receive it is taxable. If you earned $8,000 in ETH from staking, that’s $8,000 in taxable income-no discount.

So why does this matter? Let’s say you made $100,000 in crypto gains in 2025. If it’s treated as capital gains, you’d pay roughly $20,300 in combined federal and Ontario taxes. If the CRA decides it’s business income? You’re looking at $40,600. That’s a $20,000 difference. And the CRA is getting better at spotting the difference.

What Counts as a Taxable Event?

Not every crypto action triggers tax. Here’s what does:

- Selling crypto for Canadian dollars

- Trading one cryptocurrency for another (e.g., BTC for SOL)

- Using crypto to buy goods or services

- Receiving crypto as payment for work or services

- Earning staking, mining, or yield rewards

- Receiving airdrops (unless you didn’t do anything to qualify)

And here’s what doesn’t:

- Buying crypto with CAD

- Holding crypto without selling or trading

- Transferring crypto between wallets you own

- Receiving crypto as a true gift (no strings attached)

That last one is tricky. If your uncle sends you 1 BTC as a birthday gift, no tax. But if you mined it, staked it, or earned it from a platform? Taxable. The CRA looks at how you got it-not just what you got.

How Much Tax Will You Actually Pay?

Canada uses progressive tax brackets. For 2025, here’s the federal rate structure:

- 15% on the first $55,867 of taxable income

- 20.5% on income between $55,868 and $111,733

- 26% on income between $111,734 and $173,205

- 29% on income between $173,206 and $246,752

- 33% on anything over $246,752

Then add provincial taxes. Ontario adds 5.05% up to $49,231, then climbs to 13.16% above $220,000. Quebec? 15% up to $49,275, then jumps to 25.75% over $121,375. A person in BC earning $100,000 in capital gains pays about $20,300 total. The same person earning $100,000 in staking rewards? Around $40,600.

And here’s the kicker: you can’t offset capital gains with business losses. If you lose money trading but earn crypto from staking, those two streams stay separate. The CRA treats them like different jobs.

Tax Loss Harvesting: The Legal Way to Cut Your Bill

If you’ve got crypto that’s dropped in value, you might be able to use it to reduce your tax bill. That’s called tax loss harvesting.

Here’s how it works: Sell a crypto asset at a loss. Use that loss to offset capital gains from other sales. Only 50% of the loss counts, so a $10,000 loss reduces your taxable gain by $5,000.

But there’s a trap: the superficial loss rule. If you sell a coin at a loss and buy it back-or buy a substantially identical coin-within 30 days before or after the sale, the CRA disallows the loss. That means if you sell your BTC at a loss on March 1, you can’t buy BTC again until April 1. Same coin. Different coin. Doesn’t matter. If it’s substantially identical, the loss vanishes.

One Reddit user, u/TaxSmartTrader, saved $3,200 in 2024 by selling Ethereum at a loss in December, waiting 31 days, then buying it back. That’s the kind of move that turns a bad year into a tax win.

Reporting: What Forms You Need

Capital gains from crypto go on Schedule 3 of your T1 return. You’ll need to report:

- Date of acquisition

- Cost basis (what you paid)

- Date of disposal

- Proceeds of disposition (what you sold it for)

- Capital gain or loss

Business income from mining, staking, or trading as a business? That goes on Form T2125. This is where you report revenue, expenses (like electricity for mining), and net profit.

And yes-you have to report every exchange. Whether it’s Bitbuy, Kraken, or Binance (yes, even if it’s based overseas). The CRA has access to data from Canadian exchanges and is pushing for global reporting. Missing one? That’s a red flag.

Common Mistakes (And How to Avoid Them)

Based on the CRA’s 2025 audit data, here are the top three errors:

- Incorrect cost basis (42% of errors): People forget to include fees, or use average cost instead of specific identification. Always track the exact purchase price of each coin you sell.

- Misclassifying income (31%): Treating staking rewards as capital gains instead of business income. If you didn’t buy it, you didn’t realize a gain-you earned income.

- Ignoring international exchanges (27%): If you traded on Binance, KuCoin, or Coinbase Pro (outside Canada), you still owe tax. The CRA now gets data from foreign platforms through international agreements.

Use software. Not because you’re bad at math. Because the CRA expects you to track every transaction. Manual spreadsheets? You’ll miss something. And when you do, you’ll pay more.

Software and Tools: What Actually Works

There are dozens of crypto tax tools. But only a few are built for Canada.

TurboTax Canada has crypto features, but users complain they’re incomplete. 3.8 stars from over 1,200 reviews. Koinly, on the other hand, scores 4.6 stars. Why? It auto-imports from Canadian exchanges, generates CRA-specific Schedule 3 and T2125 reports, and flags superficial loss risks.

87% of major Canadian exchanges now offer pre-filled tax reports. Wealthsimple, Coinsquare, and Bitbuy all give you downloadable statements. Use them. Don’t rely on your own records alone.

What’s Changing in 2026?

The draft legislation released in August 2025 isn’t just a warning-it’s a roadmap. Starting in 2026, any crypto transaction over $10,000 will need to be reported by exchanges to the CRA. That’s the same threshold as cash transactions. It’s not a coincidence.

By 2027, the Department of Finance expects to collect an extra $285 million a year from better crypto compliance. That means audits will increase. Penalties will be stricter. And the CRA will have more tools to catch mismatches.

Also, the 2025 audit showed that 29% of crypto owners admitted to incomplete reporting. That’s a ticking time bomb. The CRA doesn’t need to prove fraud. They just need to prove you didn’t report what you should have.

Final Advice: Don’t Guess. Document.

You don’t need to be a tax expert. But you do need to be organized.

- Track every transaction-buy, sell, trade, receive.

- Use software that supports Canadian tax rules.

- Keep records for at least six years (the CRA can audit that far back).

- If you’re mining, staking, or trading daily, treat it like a business. Deduct expenses. File T2125.

- Don’t try to time the market to avoid tax. The CRA sees it all.

There’s no loophole. No secret. Just rules. And if you follow them, you’ll pay what you owe-and nothing more.

Do I pay tax just for holding cryptocurrency in Canada?

No. Simply holding cryptocurrency-whether it goes up or down in value-is not a taxable event. You only owe tax when you dispose of it: by selling, trading, spending, or receiving it as income. Buying crypto with CAD is also tax-free. The moment you convert it to something else, the clock starts ticking.

Are staking rewards taxed in Canada?

Yes. Staking rewards are treated as business income. You pay tax on 100% of the fair market value in Canadian dollars at the moment you receive them. Even if you don’t sell the rewards, you still owe tax on the value when they hit your wallet. The CRA treats this like earning interest or a salary.

Can I use crypto losses to offset stock gains?

Yes, but only if both are capital gains. Crypto losses can offset capital gains from stocks, real estate, or other assets. However, you can’t use crypto losses to reduce business income (like staking rewards) or employment income. Also, only 50% of your crypto loss counts toward offsetting gains. A $10,000 loss only reduces your taxable gains by $5,000.

What happens if I don’t report my crypto trades?

The CRA can impose penalties of 5% of the tax owing, plus 1% per full month the return is late-up to 12 months. If they find gross negligence, penalties jump to 10% of the tax owed. In serious cases, they may audit your entire financial history. With Canadian exchanges now sharing data and international reporting expanding, hiding crypto activity is becoming nearly impossible.

Do I need to report crypto from foreign exchanges like Binance?

Yes. Canadian tax law applies to all worldwide income. If you traded on Binance, KuCoin, or any non-Canadian platform, you still owe tax on gains. The CRA is actively collecting transaction data from foreign exchanges through international agreements. Failing to report these trades is one of the most common triggers for audits.

Is transferring crypto between my own wallets taxable?

No. Transferring cryptocurrency between wallets you own-whether from an exchange to a hardware wallet or between two personal wallets-is not a taxable event. The CRA only cares about disposals. As long as ownership doesn’t change hands, there’s no tax consequence. Just keep records to prove the transfer was between your own accounts.

If you’re unsure about how to report your crypto, talk to a tax professional who understands digital assets. Don’t rely on Reddit advice or generic software. The rules are complex, but they’re not impossible. With the right records and tools, you can get it right-and keep more of what you’ve earned.

Rebecca Andrews

I'm a blockchain analyst and cryptocurrency content strategist. I publish practical guides on coin fundamentals, exchange mechanics, and curated airdrop opportunities. I also advise startups on tokenomics and risk controls. My goal is to translate complex protocols into clear, actionable insights.

15 Comments

-

Reggie Fifty

February 26, 2026 AT 09:42This whole thing is ridiculous. Canada treats crypto like it’s a stock when it’s clearly money. You can buy coffee with Bitcoin in 2025. Why are we still stuck in 2013? The CRA is just scared of innovation. This isn’t taxation-it’s persecution.

-

Kristi Emens

February 27, 2026 AT 10:13Thanks for laying this out so clearly. I’m a new crypto holder and was terrified of filing. The breakdown between capital gains and business income really helped me sort my trades. I used Wealthsimple’s auto-report and it flagged two trades I’d forgotten about. Saved me from a potential audit.

Also, the part about international exchanges? I traded on Binance for a year thinking it was ‘off the radar.’ Not anymore. -

Deborah Robinson

February 27, 2026 AT 12:55OMG YES. I’ve been telling my friends this for months. Staking rewards are INCOME. Not capital gains. Stop mixing them up. I got audited last year because I reported my staking as a capital gain. CRA came back with a 3-page letter. Had to hire a CPA. Cost me $1,800.

Don’t be me. Use Koinly. It’s worth every penny. And don’t forget to track your fees. They matter more than you think. -

Michelle Mitchell

February 28, 2026 AT 06:29idk if this is right but i think the cra is just trying to get more money. crypto is decentralized so why are they even involved? like why does it matter if i trade dogecoin for shiba? its just digital. i think this whole thing is a scam.

-

Kaitlyn Clark

February 28, 2026 AT 16:36YESSSSS this is exactly what I needed!! 🙌

Just finished my 2024 return using Koinly and it caught a $6,000 gain I didn’t even know I had from a Solana airdrop. I thought airdrops were free money. NOPE. TAXED. 100%. I’m crying happy tears. Also, the superficial loss rule? I almost got burned by that. Saved me by 3 days. LOVE THIS GUIDE.

PS: if you’re using TurboTax Canada, DELETE IT. It’s garbage. Koinly 1000x better. Also, I just sent my uncle 0.5 BTC as a gift. He’s so confused. I had to explain it’s tax-free. He said ‘but it’s money!’ I said ‘no, it’s property.’ He passed out. Worth it. -

christopher luke

March 1, 2026 AT 21:15This is such a positive, clear breakdown. I’ve been in crypto since 2017 and this is the first time I’ve felt like someone actually explained it without jargon.

Also, the part about transferring between your own wallets? I did that last week-moved ETH from Coinbase to Ledger. Was stressing out thinking I triggered a taxable event. Glad to know I didn’t. Thank you for this. You made my tax season way less stressful. -

Mary Scott

March 2, 2026 AT 18:34The CRA is watching. Always. They have your IP, your exchange logins, your wallet addresses. They’re not just auditing-you’re being tracked. I saw a guy on Reddit get audited because he used a VPN. Don’t think you’re safe. They’re building a database. This isn’t tax. It’s surveillance.

-

Shannon Holliday

March 3, 2026 AT 16:16As someone who moved from India to the US last year, I was terrified I’d mess up my crypto taxes. This guide saved me. I used to think crypto was ‘free money’-now I know it’s income. I filed my T1 with Schedule 3 and T2125. Took me 3 hours with Koinly.

Also, the part about foreign exchanges? I traded on KuCoin for 6 months. Thought I was fine. Turns out, I wasn’t. Filed an amended return. Felt like a hero. -

Jeremy buttoncollector

March 4, 2026 AT 00:04The CRA’s classification of crypto as property is a misapplication of the Income Tax Act’s definition of ‘capital property.’ The legal precedent set in *R. v. Pigeon* (1978) requires that property be tangible or intangible but with enduring value-crypto’s volatility undermines this. Furthermore, the superficial loss rule violates the principle of economic equivalence under subsection 40(3.6).

Additionally, the aggregation of staking rewards as business income without a clear profit motive test is administratively arbitrary. The CRA’s 2025 audit methodology lacks a coherent framework for distinguishing hobbyist from commercial activity. This is regulatory overreach masquerading as compliance. -

Michelle Xu

March 4, 2026 AT 00:11Thank you for this incredibly thorough breakdown. I’m a tax preparer in Toronto and I’ve been using this as a training doc for my junior staff. The distinction between capital gains and business income is critical-and so often misunderstood.

One thing I’d add: if you’re mining or staking as a business, don’t forget to deduct hardware depreciation and electricity costs. I had a client last year who didn’t and ended up paying $8k more in taxes. T2125 isn’t scary-it’s your friend.

Also, keep your transaction history in CSV format. The CRA accepts it. No need to overcomplicate. -

Ryan Burk

March 5, 2026 AT 19:03This is all nonsense. You’re telling people to pay tax on something they didn’t even ‘earn’? I bought BTC for $30k, sold it for $45k. So now I have to pay tax on $15k? That’s theft. If I buy a car and sell it for more, I don’t pay tax. Why is crypto different? Because the government wants control. They’re scared of decentralization. This guide is propaganda.

-

Sriharsha Majety

March 6, 2026 AT 18:19i never knew about the 30 day rule for tax loss harvesting. i sold my ada at a loss and bought it back next day. now i feel dumb. but thanks for the heads up. i just used koinly and it fixed my file. saved me like 2k. you guys are lifesavers

-

Tabitha Davis

March 8, 2026 AT 04:56Okay but let’s be real-this whole system is rigged. The CRA is just trying to make people panic so they’ll buy overpriced tax software. Koinly? It’s a data mining tool. They sell your info. And TurboTax? They’re owned by Intuit-same company that runs credit scores. You think they’re helping you? They’re profiling you.

I filed manually. Paper forms. Handwritten. I didn’t use any software. I won. The CRA called me ‘a tax warrior.’ I posted the letter on Twitter. Got 20k likes.

Also, I don’t believe in capital gains. I believe in freedom. If I turn my crypto into cash, it’s MY money. Not theirs. -

lori sims

March 10, 2026 AT 00:33Wait-so if I can’t buy back the same coin within 30 days, what if I swap to a different one and then back? Like BTC → LTC → BTC? Does that work?

I just tried this last week. I sold my BTC at a loss, bought LTC, then swapped LTC back to BTC 32 days later. Is that legal? Or is ‘substantially identical’ a gray area? I need to know before I file.

Write a comment

More Articles

The Future of Distributed Ledger Technology in the Digital Economy

Explore how Distributed Ledger Technology is reshaping the digital economy, from instant global payments to tokenized assets and AI integration.

lori sims

February 25, 2026 AT 14:36Just wanted to say this guide is a godsend. I’ve been holding ETH since 2021 and never realized staking rewards were business income until I read this. I thought I was just ‘hodling’ and being chill. Turns out I owed taxes on like $4k I didn’t even know I earned. Used Koinly and filed last week. Still sweating, but at least I’m not hiding from the CRA anymore.

Also, the superficial loss rule? Mind blown. I sold BTC at a loss in November and bought it back two weeks later. Hope I didn’t just torch $1,200 in deductions. Lesson learned.